It may seem unfair that your friends enjoy regular holidays while you struggle to pay bills, but your 'money behaviour type' could be to blame. Experts have identified three distinct financial styles based on how people spend and save money.

The Three Money Types

The first is 'Financial Explorer'—those who are highly engaged with their finances. This group excels at budgeting, saving, and investing. 'Habitual Savers' are cautious and conscientious, prioritising traditional saving and avoiding debt. The third group, 'The Disengaged', encompasses those who do little financial planning, minor budgeting, and have hardly any savings.

The team emphasised that these behavioural profiles are not a ranking system, as each has pros and cons. Instead, they can be a useful tool to improve financial habits and boost economic security.

'There's no perfect money type here,' said co-author Dr Steffen Westermann, a financial planning lecturer at Griffith University. 'Each group does some things well and others less so.'

Study Details

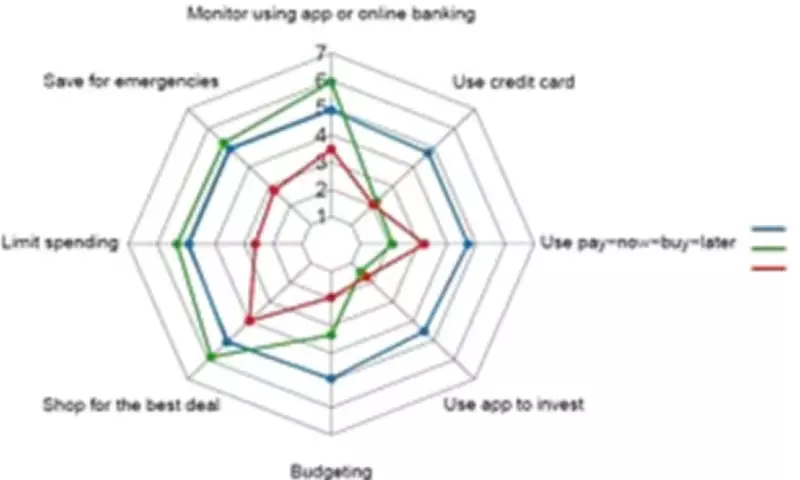

For the study, published in the Pacific-Basin Finance Journal, the researchers recruited 519 people aged between 18 and 35. Participants rated how often they engaged in certain financial habits, such as saving for emergencies, shopping for the best deal, budgeting, using apps to invest, using buy-now-pay-later services, and using a credit card. The researchers grouped participants into three clusters, showing that not all young people have the same attitude and approach to money.

1. Financial Explorers

This group frequently engages in all financial activities, including budgeting, saving, and investing. They are more likely to discuss financial matters with their partner, extended family, and friends compared to other groups. This cluster had the highest proportion of male participants but also were more likely to be overconfident about their financial skills.

2. Habitual Savers

This cluster relies on themselves rather than seeking advice from others. They tend to be more conscientious and have higher spending control, finding it easier to save leftover pay rather than spend it. 'In summary, it appears that Habitual Savers are a group of young adults with personalities and perceptions that may enable them to sacrifice current impulses to maximise future utility,' the team wrote. However, they might miss opportunities to build long-term wealth.

3. The Disengaged

This group is least likely to engage in financial activities, except for buy-now-pay-later schemes. 'These financially disengaged young adults do not appear to have developed any clear financial habits,' the researchers wrote. 'At most, they sometimes shop for the best deal, occasionally monitor their finances, and use buy-now-pay-later services.' Those in this category are also more likely to experience financial stress.

Implications for Financial Education

Lead author Dr Jennifer Harrison, from Southern Cross University, said the findings have important implications for financial education, policy, and support services. 'One-size-fits-all financial literacy programs are unlikely to be effective,' she said. 'Young people are not a homogeneous group when it comes to money. They bring different habits, confidence levels, and social influences into their financial lives.'

The research suggests more tailored approaches could better support different groups. For example, helping Financial Explorers better assess risk and navigate information sources, supporting Habitual Savers to build long-term wealth through appropriate investing, and providing The Disengaged with simple, low-effort tools to reduce financial stress and build basic habits.